The 2026 Architectural Transformation: Blockchain Integration and Revenue Frontiers in Global Banking

The global financial landscape in 2025 has reached a definitive inflection point where decentralized ledger technologies (DLT) have migrated from experimental pilot phases into the core of operational banking systems. This transition is not merely a technological upgrade but a fundamental shift in the paradigm of trust and value movement. As global spending on artificial intelligence and blockchain-related infrastructure approaches the $1 trillion mark, the banking sector is hollowing out legacy cores to accommodate real-time, programmable, and transparent financial instruments. The convergence of regulatory clarity in approximately 80% of major jurisdictions with the arrival of high-throughput Layer-1 and Layer-2 blockchains has fundamentally altered expectations regarding transaction speed, cost, and liquidity management.

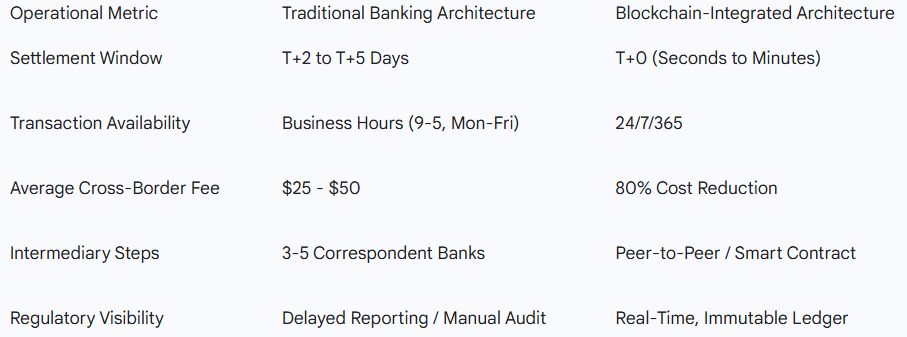

Traditional banking ecosystems are currently burdened by systemic inefficiencies that create significant "dead capital" and operational drag. Traditional international wire transfers are notoriously slow, often requiring three to seven business days for finality due to the reliance on multiple intermediary correspondent banks. These legacy rails introduce opacity, with fees ranging from $25 to $50 per transaction, and a lack of real-time visibility into the status of funds in transit. The cost of maintaining these systems is further exacerbated by the redundant nature of Know Your Customer (KYC) and Anti-Money Laundering (AML) processes, which are traditionally performed in silos by every participating institution. Analysts estimate that more than two in five U.S. banks still operate on legacy back-end systems designed nearly four decades ago, which are characterized by batch processing and high maintenance overhead.

The Crisis of Legacy Intermediation and Structural Friction Points

The inefficiency of the current banking architecture is most visible in the "payment float," where billions of dollars in consumer and corporate payments are locked up every weekend globally due to the constraints of traditional banking hours. This trapped liquidity represents a massive opportunity cost for merchants and businesses who cannot redeploy capital or start generating interest revenue until the funds settle days later. In the current high-interest-rate environment, the inability to earn yield on this float translates into several billion dollars of forgone interest income annually.

Beyond the speed of transactions, the banking sector faces a crisis in data integrity and reconciliation. Because each financial institution maintains its own siloed ledger, the process of verifying a transaction involves constant communication and manual reconciliation between disparate systems. This not only introduces human error but also creates a "trust deficit" that requires expensive third-party validators to bridge. Blockchain technology functions as a "code-based trusted intermediary," encoding the rules of engagement into self-executing programs known as smart contracts. This shift allows for "self-regulation," where institutions can interact through a shared ledger that seamlessly adheres to predefined conditions, thereby reducing the dependency on cumbersome regulatory oversight.

Domain Analysis: Reimagining Global Payments and Remittances

Cross-border payments represent the most immediate domain for blockchain improvement. The traditional correspondent banking model is increasingly viewed as unsuitable for a digital-first global economy. In 2024, global cross-border payments totaled over $40 trillion, with a projected annual increase of 5% until 2027. Despite this volume, the infrastructure remains fragmented. Blockchain-based payments elegantly solve these problems by settling transactions in minutes rather than days and reducing costs from dollars to pennies.

One of the strongest practical business cases is the use of stablecoins like USDC and USDT for B2B settlements. Businesses are increasingly turning to stablecoins to settle international invoices with partners and suppliers, bypassing Swift fees and mitigating exposure to foreign exchange (FX) volatility. For example, a tech startup in the UK can instantly pay a freelance developer in Argentina using stablecoins, bypassing traditional banking rails and ensuring on-time payments even on weekends. This is particularly vital in high-inflation markets where immediate access to digital dollars protects earnings from local currency depreciation.

The revenue opportunity for banks in this domain is substantial. Instead of losing transaction volume to unregulated offshore platforms, banks can offer P2P crypto payments through their existing mobile banking apps. By charging a nominal transaction fee of 0.2% to 0.5%, banks can generate significant income while providing customers with enhanced security and insurance that crypto-native firms often lack. Furthermore, as B2B cross-border payments on blockchains are estimated to soon account for 11% of total international payments, banks can monetize the provision of "on-ramp" and "off-ramp" services, converting fiat to digital assets and back for their corporate clients.

The Rise of Programmable Money and Bank-Side Programmability

A profound evolution in the banking ecosystem is the shift from static transactions to "programmable finance." This involves integrating conditional logic directly into the digital currency or the payment process. The distinction between "programmable money" (where logic is built into the asset) and "programmable payments" (where logic triggers the movement of existing funds) is central to new banking revenue models.

Smart Escrow and the Monetization of Payment Float

Traditional escrow services are often cost centers, requiring manual review and charging 1% to 3% in fees while capital sits idle. Smart escrow, powered by blockchain and stablecoins, transforms this into a revenue-generating opportunity. Smart contracts automatically hold and release funds based on predefined milestones—such as shipment confirmation verified via IoT sensors or quality checks.

The critical business case for banks lies in the "yield-earning escrow." While funds are held in the smart contract, they can be deployed into yield-generating protocols or secure DeFi platforms, earning an APY of 6% to 9%. For a $500,000 components shipment with a 60-day window, this can generate between $12,000 and $18,000 in yield—money that traditional escrow systems leave unproductive. Banks can monetize this by capturing a spread of the generated yield (e.g., sharing 40-60% with the customer) while providing a "zero-fee" payment service to attract more volume.

Bank-Side Programmability for Corporate Treasury

Leading institutions like JPMorgan are developing "bank-side programmability," where corporate clients can deploy their own business logic directly within the bank's system. This allows for the automation of complex treasury management techniques, such as "target balance" funding. In this model, the bank's system automatically executes transfers based on the client's predefined rules, such as moving funds to a specific jurisdiction as soon as a balance threshold is reached or triggering margin payments when collateral levels fall below requirements.

This capability creates a "closed-loop financial ecosystem" where money never needs to leave the blockchain, allowing banks to simultaneously transform into custodians, wealth management supermarkets, and credit gateways. The value for the bank is no longer just in individual transaction fees, but in becoming the essential infrastructure for "autonomous finance".

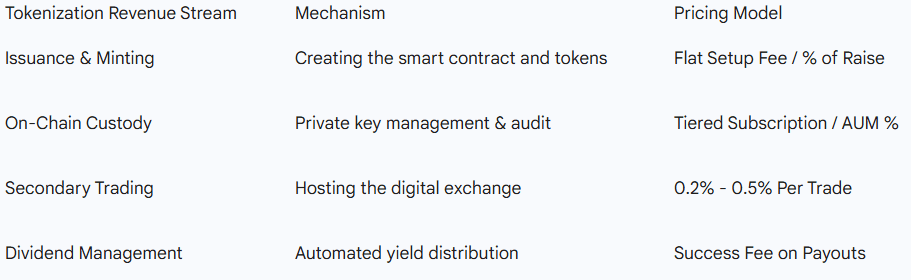

Revenue Pillar: Tokenization of Real-World Assets (RWA)

The tokenization of financial and physical assets is projected to reach a $16 trillion market value by 2030, representing roughly 10% of the global economy. This process involves converting rights to an underlying asset—such as real estate, gold, treasury bills, or art—into digital tokens on a blockchain. For banks, this opens up massive revenue streams through "Tokenization-as-a-Service" (TaaS).

Fractional Real Estate Ownership

Real estate is historically illiquid and requires significant capital. Tokenization divides a single property into multiple parts using fungible tokens, allowing investors to buy and sell small units 24/7. Smart contracts handle the automated distribution of rental income and dividends, reducing administrative overhead. Banks can monetize this by charging for issuance, management, and custody of these fractional shares, while also offering "white-label" tokenization infrastructure to proptech startups.

Digital Gold and Commodity Liquidity

In markets like the UAE, Indian expats are moving from physical gold to digital gold to avoid high import duties (13.75%–16.5%) and logistical risks. Digital gold platforms integrated with blockchain provide immutable proof of ownership and real-time pricing. Banks can act as the "independent custodian," charging for the secure vaulting of the underlying physical gold while facilitating the trading of the digital tokens. This model provides "instant liquidity" for an asset class that was traditionally difficult to move across borders.

The Institutional Turn: Repo Markets and Bond Issuance

Institutional adoption is accelerating in the fixed-income sector. Platforms like Goldman Sachs’ GS DAP™ and JPMorgan’s Kinexys are tokenizing debt instruments to reduce the settlement cycle from days to minutes. This "atomic settlement" reduces counterparty and liquidity risk, as the payment and the asset transfer happen simultaneously. Banks can generate revenue by facilitating these high-value interbank trades and providing "liquidity on demand" through tokenized inventory that can be used as collateral for instant loans.

Modernizing the Compliance Stack: Shared KYC and AML

One of the most expensive friction points in banking is the redundancy of identity verification. Currently, a customer's identity is verified separately at every institution, leading to billions in administrative costs. Blockchain-enabled KYC allows for a "shared digital identity" where a customer is verified once and their credentials, encrypted and shared with consent, are accepted everywhere across the network.

Financial institutions in Spain and other parts of Europe are already leveraging the European Blockchain Services Infrastructure (EBSI) to support cross-border KYC. This "absorptive capacity" allows banks to quickly assimilate external knowledge about customer identities and regulatory requirements, reducing duplication of efforts. The business case for banks here is two-fold:

Operational Savings: Dramatic reductions in onboarding time and compliance labor costs.

KYC-as-a-Service: Verified banks can charge a fee to other institutions or fintechs for accessing their verified customer database, essentially monetizing their "trust" and compliance rigor.

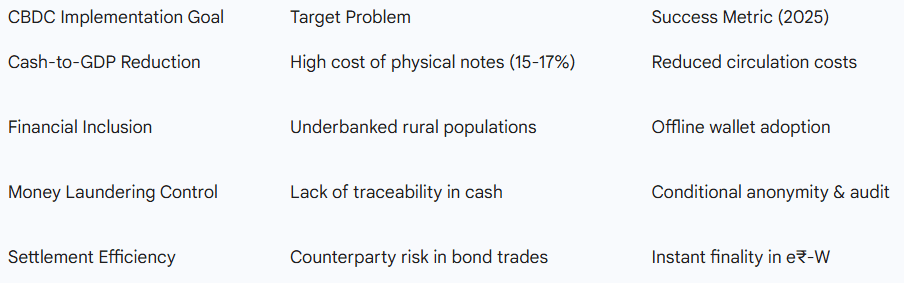

The Indian Case Study: e-Rupee and the National Blockchain Strategy

India's approach to blockchain in banking is unique, characterized by a sovereign-backed integration into the "India Stack". The Reserve Bank of India (RBI) launched the e-rupee (CBDC) pilot in late 2022, and by March 2025, the circulation has surged to over ₹1,016 crore. The e-rupee is designed to complement existing digital success stories like the Unified Payments Interface (UPI), which handles 85% of digital transactions.

Retail vs. Wholesale Implementation

The e-rupee is being tested in two distinct segments:

Wholesale (e₹-W): Used by financial institutions to settle bond trades and high-volume interbank transactions. By eliminating the need for collateral to cover settlement delays, e₹-W significantly improves the productivity of the interbank market.

Retail (e₹-R): Distributed via wallets provided by banks, it functions as a digital equivalent of physical cash. It offers features like "offline functionality," allowing users in rural areas with poor internet to make payments—a critical tool for financial inclusion.

Practical Business Case: Programmable Subsidies

The most disruptive feature of the e-rupee is its programmability. Government subsidies, such as those for fertilizer or seeds, can be sent directly to a farmer’s wallet but "locked" for specific purchases only. This ensures that public funds are used for their intended purpose, reducing corruption and administrative leakage. Banks can monetize this by partnering with government agencies to manage these programmable disbursement programs and providing the underlying wallet infrastructure.

Technical Architecture: Bridging Blockchain with Core Banking Systems

For blockchain to improve the banking ecosystem, it must be integrated with the existing legacy architecture, particularly the Core Banking System (CBS). Most modern implementations follow a "layered architecture".

The Three-Layer Integration Model

Frontend Applications Layer: This includes mobile apps and web portals where users interact with their accounts. Standardized, stateless APIs (like those used in UPI) allow these apps to communicate with the payment rail without needing to know the underlying ledger's complexity.

Middleware Business Services Layer: This tier is the most critical for blockchain integration. It handles payment address creation, authentication, routing, and "queuing infrastructure" to ensure transactions are atomic. Blockchain is integrated here as an "additional module" that provides an irrefutable transaction trail and manages smart contract logic.

Backend Banking Integrations Layer: Instead of forcing banks to replace their entire CBS—which is a high-risk, multi-year endeavor—NPCI and technology partners use "customizable adapters". These adapters allow the CBS to talk to the blockchain ledger in real-time while keeping the existing software for balance management and reporting intact.

Security and Verification Innovations

To ensure security, banks are combining DLT with advanced biometric verification. For instance, some Indian pilot systems use "three layers of verification," including multi-user facial authentication that is cross-referenced with the blockchain-stored identity. This ensures that even if a mobile device is stolen, the sensitive financial identity remains secure. The use of "Consortium Blockchains"—where only a group of trusted banks act as validator nodes—is preferred over public chains to maintain privacy and high transaction throughput.

Regulatory Dynamics and the Shift Toward "VDA as Property"

The regulatory landscape in 2025 is defined by a shift away from bans toward "risk-based oversight". In October 2025, the Madras High Court issued a landmark ruling recognizing Virtual Digital Assets (VDAs) as a form of "property" under Indian law. This means that crypto assets, while intangible, are now capable of being owned, held in trust, and subject to proprietary protection similar to movable property.

For banks, this legal clarity is a massive catalyst. It allows them to:

Hold Assets in Trust: Banks can now legally offer digital asset custody with a clear fiduciary duty to their clients.

Provide Proprietary Protection: Courts can now grant injunctive relief to protect digital property from value erosion during litigation.

Enhance Consumer Protection: Because VDAs are classified as "goods," they fall under the Consumer Protection Act, allowing for recourse in case of service deficiencies.

In other jurisdictions like the US and EU, regulators are fast-tracking a reassessment of Basel Committee rules to allow banks to engage more deeply with stablecoins on public blockchains. This softening of regulatory attitudes is expected to drive even more institutional momentum into 2026.

Strategic Business Cases for Immediate Adoption

To capitalize on blockchain, banks should move past pilot programs and into "production-ready" systems that address existing pain points.

Case 1: The "Creator Economy" Payout Engine

The creator and gig economy is expected to approach $500 billion by 2027. These workers often operate across borders and require instant payouts. A bank could build a dedicated payout engine using stablecoin rails, allowing platforms like YouTube or Upwork to pay creators instantly in USD stablecoins. The bank makes money by charging the platform for the bulk payout service and by offering the creators high-yield digital savings accounts for their earnings.

Case 2: SCF-EPTI (Supply Chain Finance)

Traditional supply chain finance is plagued by paper-based transfers and slow net-30 or net-90 payment cycles. By tokenizing inventory and using smart contracts, banks can create "SCF-EPTI" (Electronic Programmable Trust Infrastructure). When a shipment hits a specific milestone, a portion of the payment is automatically released. This provides SMEs with immediate liquidity and reduces the credit risk for the bank, as every pallet has a "digital twin" on the ledger that everyone can see and verify in real-time.

Case 3: NRI Wealth Preservation via Digital Gold

For the millions of Non-Resident Indians (NRIs) in the Middle East, traditional gold is a key store of value but a logistical nightmare to bring home. A bank could offer a "Digital Gold SIP" (Systematic Investment Plan) that allows NRIs to accumulate gold tokens on a blockchain. The gold is stored in the bank's vaults in GIFT City, and the user can either liquidate the tokens instantly for cash or redeem them for physical gold in India. The bank earns from the storage fees, the trading spread, and the currency conversion when the user liquidates their position.

Challenges to Implementation and Risks

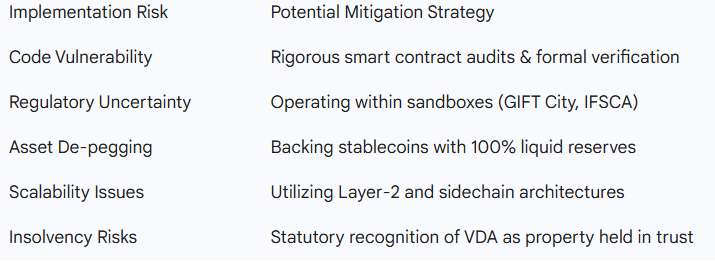

Despite the benefits, several hurdles remain. "Regulatory arbitrage" is common, where firms relocate to more favorable legal systems, complicating the determination of applicable law during insolvency. In the case of the WazirX cyberattack, the court held that the exchange could not "socialize the losses" and had a fiduciary duty toward the assets held in its custody. This highlights the legal risks banks must manage when entering the space.

Technologically, the "decentralized architecture of blockchain" can sometimes be slower than a centralized CBS. Banks must design "hybrid systems" that provide faster synchronization while maintaining the immutability of the chain. Furthermore, "smart contract vulnerabilities" remain a risk; an error in the code can lead to irreversible loss of funds. Therefore, banks must invest heavily in cybersecurity audits (like CERT-In in India) and "fit-and-proper" certifications for their digital asset partners.

Conclusion and the Path to Autonomous Finance

By the end of 2025, blockchain is no longer just another application in the banking world, it is becoming a built-in layer of the financial operating system. The technology has moved beyond text-based transactions into "agentic systems" where AI and blockchain work together to automate complex financial multi-step tasks. For banks, the era of making money solely from transaction fees is coming to a close. The new revenue frontier lies in "intelligent capital deployment," "trust-as-a-service," and the creation of "liquid, tokenized markets" for previously dead assets.

The "Coding Cash" revolution is redefining how money moves, ensuring that it is as fast, flexible, and global as the internet itself. Institutions that "hollow out the core" and integrate DLT into their middleware today will be the ones to lead the $16 trillion digital economy of tomorrow. The question is no longer whether programmable money will supplement traditional payments, but how quickly banks can recognize that optimizing old systems cannot compete with the fundamentally new capabilities of on-chain finance. Strategic focus must remain on solving real-world friction—speeding up the $40 trillion payment flow, unlocking the $30 billion weekend liquidity gap, and providing secure, regulated pathways for the next generation of digital-native investors.